When you buy bike insurance, you’ll see one term you’ll keep seeing: IDV. Many people ignore it while purchasing a policy, but it actually plays a big role when you make a claim. If you don’t understand IDV properly, you might end up either overpaying your premium or getting less money during a loss.

Let’s break it down simply and clearly.

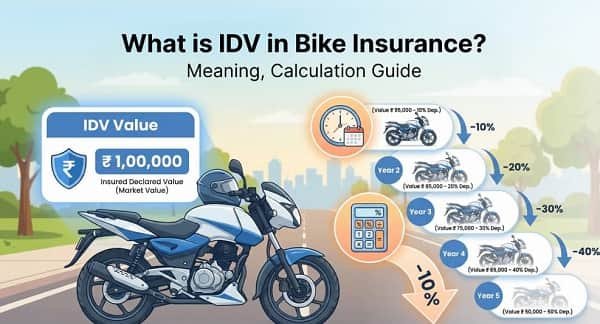

What Is IDV in Bike Insurance?

IDV stands for Insured Declared Value.

It is the current market value of your bike as decided by the insurance company. In simple words, it’s the maximum amount you will receive if your bike is:

- Stolen

- Completely damaged (total loss)

Think of IDV as the real worth of your bike at present, not the price you originally paid.

How IDV Is Calculated

IDV is not random. It is calculated based on a few standard factors:

1. Manufacturer’s Selling Price

The starting point is the bike’s ex-showroom price (without registration and insurance costs).

2. Depreciation

Every year, your bike loses value. This is called depreciation. Insurance companies follow a fixed schedule:

- Up to 6 months: ~5% depreciation

- 6 months to 1 year: ~15%

- 1–2 years: ~20%

- 2–3 years: ~30%

- 3–4 years: ~40%

- 4–5 years: ~50%

So, the older your bike, the lower the IDV.

3. Accessories (Optional)

If you’ve added extra accessories, such as alloy wheels or special fittings, their value may be included separately.

Why IDV Is Important

Many people just pick the cheapest insurance. That’s where mistakes happen. IDV directly affects two things:

1. Your Claim Amount

If your bike is stolen or completely damaged, the insurance company pays up to the IDV.

- Low IDV = lower claim

- High IDV = better compensation

2. Your Premium

Premium is linked to IDV:

- Higher IDV → higher premium

- Lower IDV → lower premium

So it’s a balance. You don’t want to go too low just to save money.

Example to Understand IDV

Let’s say you bought a bike for ₹1,00,000.

- After 2 years, depreciation reduces its value by around 30%

- New IDV = around ₹70,000

Now, if your bike gets stolen, you’ll receive around ₹70,000 (not ₹1,00,000).

That’s why IDV matters—it reflects the current reality, not past cost.

What happens if you choose the wrong IDV

This is where many people go wrong.

Choosing Low IDV

- Lower premium

- But you’ll get less money in case of total loss

- Not ideal if your bike is still valuable

Choosing High IDV

- Higher premium

- But better claim amount

- However, insurance companies won’t allow unrealistically high values

The best approach is to choose an IDV that is realistic and close to market value.

IDV vs Market Value – Are They the Same?

They are very close but not the same.

- IDV is calculated using standard depreciation rules

- Market value depends on demand, condition, and location

Still, in most cases, IDV gives a fair estimate of your bike’s worth.

IDV in Total Loss vs Partial Damage

It’s important to understand this clearly:

Total Loss / Theft

You get the full IDV amount (after any deductibles).

Partial Damage

IDV is not directly paid. Instead:

- The repair cost is covered

- Depreciation on parts is applied

So IDV mainly matters in major loss situations.

Can You Change IDV?

Yes, most insurers allow some flexibility while renewing your policy.

You can:

- Slightly increase IDV (within limits)

- Slightly decrease IDV

But don’t go too extreme. Insurance companies usually give a range, and staying within that is safer.

Tips to Choose the Right IDV

Here are some practical tips:

- Don’t unthinkingly go for the lowest premium

- Check your bike’s resale value online

- Keep IDV close to the realistic market value

- Avoid over-inflating just for higher claims

- Review IDV every year during renewal

A balanced IDV gives you peace of mind without overpaying.

Common Myths About IDV

“Higher IDV means guaranteed full payment.”

Not always. Conditions, deductibles, and policy terms still apply.

“Lower IDV saves money, so it’s better.”

Short-term savings, but risky in case of theft or total loss.

“Old bikes don’t need proper IDV.”

Even old bikes have value. Choosing too low can hurt you later.

Final Thoughts

IDV might look like just another number in your insurance policy, but it quietly controls how much protection you really have. It decides what you’ll get when things go wrong.

A smart bike owner doesn’t just buy insurance—they understand it.

So next time you renew your bike insurance, don’t skip the IDV part. Take a minute to check the value and choose wisely. It can make a big difference when you need it the most.